The National Association of College and University Business Officers (“NACUBO”) and TIAA recently released their 2021 “Study of Endowments.” This highly anticipated annual study provides a report of university endowment investment allocations and returns.

Overall, university endowments had a good 2021 fiscal year (which for endowments ended on June 30, 2021); the average endowment notched just over a 30% gain. On the other hand, a simple 70/30 indexed portfolio returned 29% in fiscal year 2021, and the similarity of returns begs the question: Is it worth the complexity, additional fees, and taxes for an individual investor to seek to emulate the endowment model of investing?

Digging into the data in the NACUBO-TIAA study provides some answers.

How the Endowment Model Works

The Endowment Model (also called the Yale Model) was developed by David Swenson, Yale’s longtime chief investment officer, and popularized in his 2000 book, Pioneering Portfolio Management. The primary characteristics of the Endowment Model are:

- Broad diversification across asset classes

- Low allocations to assets with low expected returns, such as fixed income and commodities

- High allocations to illiquid assets such as hedge funds, private equity, private real estate, and venture capital.

Beginning in the mid-1980s, Swenson (who died last year) led Yale’s endowment to eye-popping returns. Its 11.3% annualized return over the past 20 years makes it the top performing endowment for that period.

Since its popularization in the 2000s, the Endowment Model has taken the investment industry by storm. Tax-exempt investors such as pension plans and foundations, as well as taxable high net worth individuals, have sought to emulate Yale’s returns by tilting their portfolios away from traditional stocks and bonds and towards illiquid alternative investments.

But Yale’s returns aren’t just about its philosophy and allocation; Yale’s endowment employs 30 investment and legal professionals, has numerous strategic partnerships, and a name that gives all of them access to top investment managers. While other endowments have delivered stellar, Yale-like returns (such as Washington University in St. Louis which notched the top endowment return of 65% for fiscal year 2021 and was the second highest performer in fiscal year 2020), most endowments have struggled to keep up with Yale and other top performing endowments.

Into the Allocation Weeds

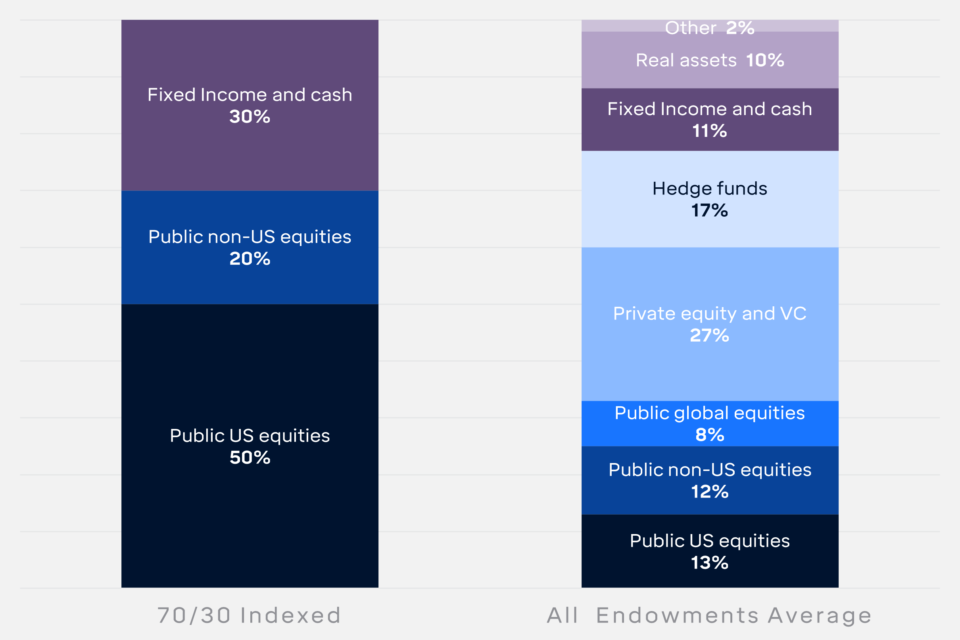

The NACUBO-TIAA study provides data on 720 university endowments, ranging from the 29 with less than $25 million to the 136 with greater than $1 billion. The data shows that the larger endowments have made greater allocations to alternative asset classes like hedge funds, private equity, venture capital, and real assets, while the smaller endowments have relatively larger allocations to public stocks and bonds. All 720 endowments roll up to the allocation on the right side of the chart below; the 70/30 model is on the left:

Allocation of 70/30 Index Portfolio and All Endowments

ST. LOUIS TRUST & FAMILY OFFICE; DATA FROM 2012 NACUBO-TIAA STUDY OF ENDOWMENTS

In terms of passive versus active, endowments heavily utilize active managers for 70% of their domestic public stocks and 90% of their international equities. Of course, all their private equity, venture capital, and real asset investments are active as well.

Comparing Endowment Returns to a 70/30 Indexed Portfolio

To judge whether the illiquidity, complexity, and fees inherent in the Endowment Model are worth it for universities, let’s compare endowment returns to those of a simple portfolio of 70% publicly traded stocks and 30% bonds and cash.1

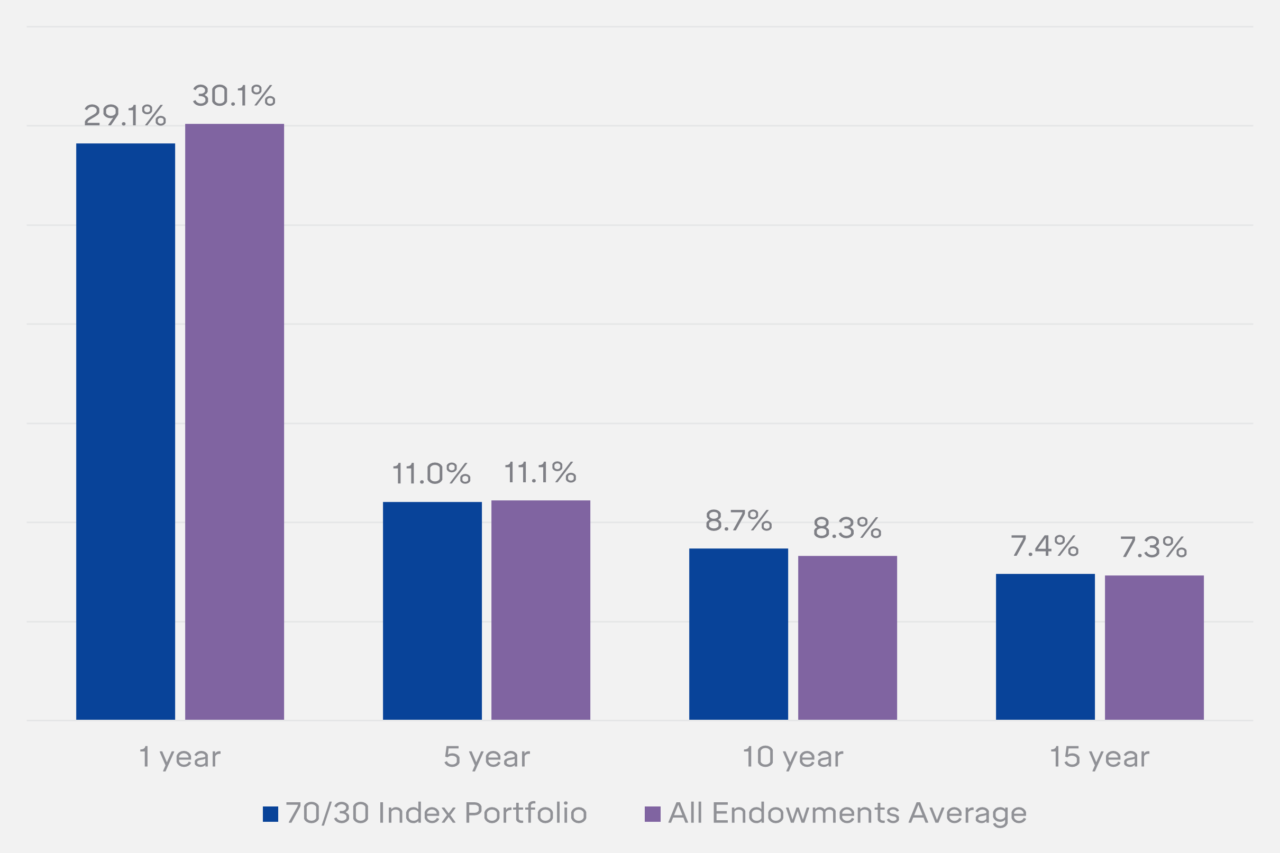

As previously noted, endowments and a 70/30 index portfolio have generated indistinguishable returns, and not just in 2021. The median endowment in the NACUBO-TIAA study is slightly higher than the 70/30 index portfolio over the past 1 and 5 years, but slightly less over 10 and 15 years. See chart below.

Annualized Returns of 70/30 Index vs. All Endowments

*15-year endowment figure is the mean of all endowments.

ST. LOUIS TRUST & FAMILY OFFICE; DATA FROM 2012 NACUBO-TIAA STUDY OF ENDOWMENTS

Digging more deeply into the returns data reveals:

- There was a big dispersion among endowment returns in fiscal year 2021; the 95th percentile manager returned 43% while the 5th percentile returned just 20%.

- In general, larger endowments performed better than smaller endowments over both the 1-year period, as well as the longer periods. While the study offers no reason for that, the higher returns of large endowments are likely due to their more aggressive allocations to private equity and venture capital (and better access to top funds in those asset classes) combined with a lower allocation to bonds.

- Overall, the active public stock investment managers used by the endowments underperformed the market.

- Speaking of the market, the S&P 500 has had an amazing 15-year run — returning just under 11% per year. Not surprisingly, both endowments and the 70/30 portfolio failed to keep up as investment in most anything other than US stocks over that time would trail the S&P.

- Interestingly, about one-third of endowments have student-managed portfolios, and those portfolios outperformed the endowment average with a 35% return in fiscal 2021.

Takeaways for Individual Investors

Yale’s, Washington University’s, and the returns of other top endowments demonstrate that the Endowment Model can deliver exceptional returns. However, the NACUBO-TIAA study indicates that many universities are spending a lot of time, resources, and expense trying to emulate the top performing endowments without much to show for it given that the average endowment return is indistinguishable from a 70/30 index portfolio. For individual investors, this should be a red flag: If endowments, with all their resources and professional staff, aren’t doing any better as a group than a simple index portfolio, then the odds also are against individual investors matching the returns of the top endowments.

An additional factor is taxes. Endowments are tax exempt while individual portfolios (other than retirement accounts) throw off taxes. If endowments paid taxes, they would invest in a more tax efficient manner. In their paper What Would Yale Do If It Were Taxable?, Patrick Geddes, Lisa R. Goldberg, and Stephen W. Bianchi concluded that if Yale paid taxes, it would alter its investment allocations by:

- Eliminating active equity managers and hedge funds,

- Reducing allocations to private equity and real assets, and

- Increasing the percentage in index funds and bonds.

In other words, Geddes and his colleagues concluded that Yale would invest closer to a 70/30 index portfolio than the Endowment Model if it had to pay taxes… like you.

1 Specifically, the 70/30 portfolio consists of, 5% 3-month T-Bill, 25% Barclays 1-10 Municipal Bond Index, 37% Russell 1000, 12% Russell 2000, 15% MSCI EAFE, 2% MSCI EAFE Small Cap, and 4% MSCI Emerging markets. The portfolio is rebalanced annually.